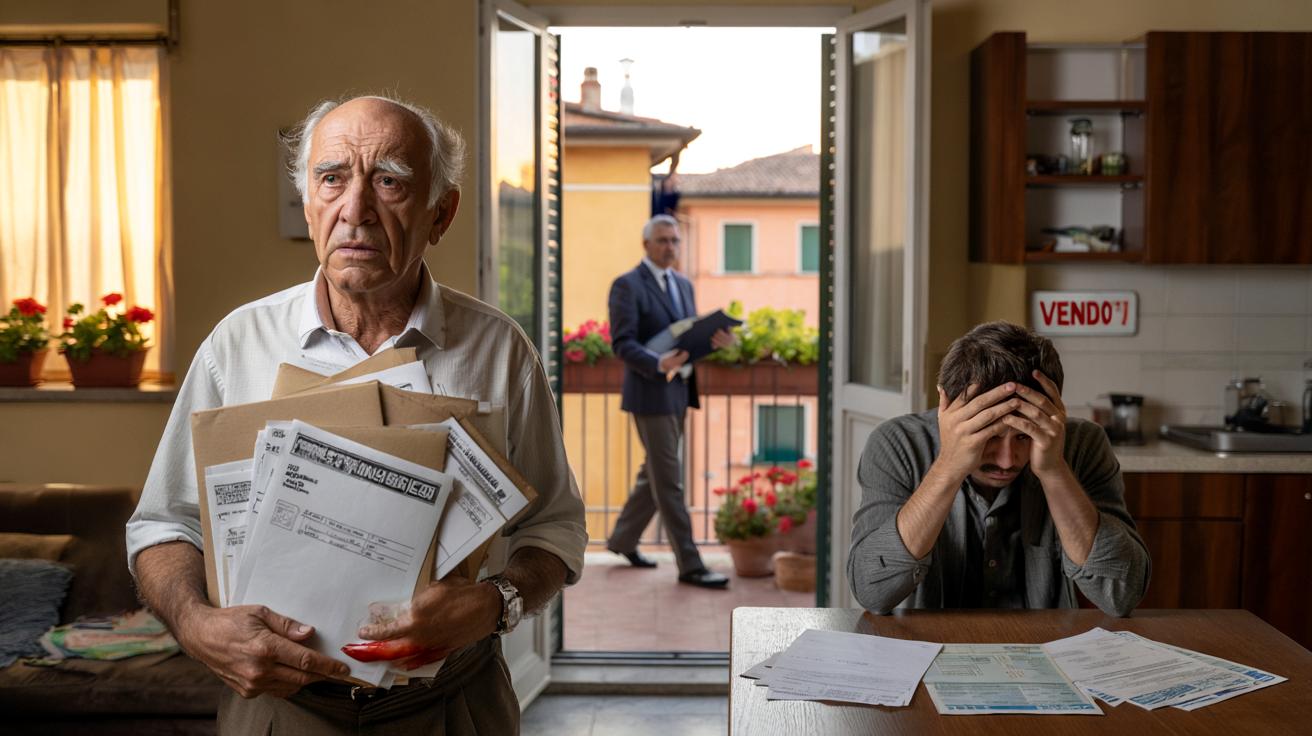

The neighbours say they used to see him every morning, watering the geraniums on the balcony of a modest apartment in the outskirts of Bologna. A retired metalworker, 72 years old, always the first to greet the postman, always a small joke ready for the kids going to school. Then, one day, the mail changed. No more postcards, only brown envelopes. Registered letters. Stamps with the cold logo of the Agenzia delle Entrate.

Behind those envelopes, a story that many Italian families know too well: a son in his forties without a stable job, a father who offers himself as guarantor for a loan, a bank that says yes, the dream of a restart. And then the collapse.

Now the tax office wants to auction off the house. And half of Italy is asking the same question: who really made the mistake?

Pensioner, son and loan: how one “favour” turned into a nightmare

The story, reconstructed by several local newspapers, begins in a very ordinary way. The son, 44, bouncing between short-term contracts and months on unemployment, asks his retired father to help him get a personal loan. On his own, no bank would approve it. With the pensioner’s house as collateral, suddenly the doors open. The family thinks it has won a small victory, one of those compromises you accept when the economic crisis becomes a kind of permanent weather forecast.

For a while, everything seems under control. Then the jobs become fewer, the instalments pile up. First one late payment, then three. The letters arrive. The phone calls, more and more insistent. Until the tax authority finally steps in.

The decisive twist comes when unpaid amounts, penalties and interests are transferred for collection. The “favour” of a father transforms into a debt machine with no brakes. The retired man, convinced he has done the right thing, discovers he is the one officially responsible. The son disappears from the paperwork. On the mortgage contract, the signatures that really count are his.

At that point, the story leaves the living room and ends up on social media and talk shows. On one side, those who accuse the son of having “destroyed” the family. On the other, those who point the finger at the banks and a fiscal system that seems relentless with the weak and flexible with the strong. The country splits in two, but the eviction procedure goes on undisturbed.

From a legal perspective, the mechanism is cruel but simple. When you act as guarantor or pledge your home, you are not “helping” symbolically. You are putting yourself in the front line. If the primary debtor cannot pay, enforcement starts with your assets. Cold law, no sentiment.

There is another harsh detail: the pensioner had underestimated the time factor. A debt that might seem manageable on paper becomes a trap when interest, penalties and collection costs accumulate. Suddenly the numbers run faster than a modest pension. *A promise made in the name of love collides with an arithmetic that does not bargain.*

At that point, everyone feels entitled to judge. But no judgement cancels an attachment order.

➡️ “Ho smesso di modificare questa ricetta perché è già perfetta così”

➡️ “I cambi di routine mi destabilizzano”: la psicologia spiega il bisogno di struttura

➡️ Cosa significa rifare il letto appena svegli, secondo la psicologia

➡️ “Ho scelto un ruolo poco visibile e oggi guadagno 45.000 euro l’anno”

What this case reveals about Italian families, money and guilt

Behind the headlines, there is something more uncomfortable than the scandal itself. This story exposes how Italian families work when money gets tight. Parents of the boomers’ generation often feel they are the last safety net, the human bank that never says no. They grew up with the idea that owning a house is sacred, yet they are the first to offer that same house as a shield for their children.

The son, like many of his age, has grown up in a labour market without guarantees. Short contracts, internships, “collaborations”, a CV full of fragments. He doesn’t ask for a loan to buy a Ferrari, but to breathe, to get married, to launch a micro-business. The line between necessity and imprudence becomes dangerously thin.

We’ve all been there, that moment when a relative asks for help and saying no feels almost like a betrayal. In this case, the pensioner, with a modest monthly cheque and rising bills, says yes. Not because he is naive, but because he belongs to a culture where you sacrifice yourself for your children, whatever the cost. He signs documents full of small print that neither he nor his son truly understands.

Banks, on the other hand, move in a world where spreadsheets have more weight than family dinners. The risk? Moved from an unstable worker to a property-owning pensioner, the perfect client: house paid off, steady income. For the financial institution, it’s almost a risk-free operation. For the family, it is Russian roulette.

The harshest split is not only between state and citizen, or between bank and debtor. It is at the dinner table. Some accuse the son of having exploited his father. Others say the real trap is a system that forces a 70-year-old to sign to remedy the failures of politics and work. Both positions have a piece of truth.

Let’s be honest: nobody really reads every single clause they sign in these situations. Between trust, hurry and fear of losing an opportunity, signatures become a leap of faith. The tax office, of course, does not deal in feelings. **A debt is a debt**. **A guarantee is a guarantee**. **A house is an asset**. These three dry facts collide with something much bigger and messier: love, shame and the terror of ending up on the street after a lifetime of work.

How not to repeat this tragedy: concrete steps and emotional traps

One practical lesson from this story is brutally simple: never sign as guarantor, or put your home up as collateral, without an external check. Not from the bank advisor, but from someone who has nothing to gain: a consumer association, a union tax service, a lawyer, even a trusted accountant. One hour of consultation can change an entire life.

There is another gesture that sounds small but is powerful: asking for everything in writing and bringing it home. Reading and rereading in calm, maybe with a younger relative who is used to sorting through bureaucracy. Only then, if the numbers still add up, going back to sign. The time between “I’ll think about it” and “I’ll sign” is where a disaster can be avoided.

The most frequent mistake, and the most human, is treating money within the family as if it were outside of reality, like a private universe with different laws. “He’s my son, he’ll never leave me stranded.” “The bank would never confiscate the home of an elderly man.” Thoughts like these sound comforting, but they are fantasies. The system does not distinguish between generous and selfish people, between model fathers and absent parents. It only sees contracts.

That doesn’t mean closing your heart. It means not confusing love with blind financial trust. Saying no to a risky loan can be an act of protection, not of abandonment. And if the shame feels unbearable, talking about it with others, before signing, often reveals that many are struggling with the same dilemmas.

“Dad, they’re not going to take your house, don’t worry,” the son is reported to have said before the contract. Those words, probably sincere at the time, now sound like a ghost echoing in the corridor as the eviction date approaches. In many comments online, people write the same sentence: “I would have done exactly what that father did.” That’s the scariest part.

- Ask for a full simulation of worst-case scenarios: what happens if the debtor does not pay for 3, 6, 12 months?

- Calculate the impact of the debt on a single pension, not on the “ideal” income of the family.

- Set a hard limit: I will not risk my primary home, under any condition.

- Consider non-financial help first: hosting the son, sharing expenses, helping with childcare or job hunting.

- Talk openly about failure: what do we do, together, if the project financed by the loan doesn’t work?

Beyond blame: what this story says about all of us

The retired man of Bologna could be many fathers and mothers across Italy. Different town, same balcony, same fear when someone rings the doorbell and you don’t know if it’s the postman or another officer with a paper to sign. His story has gone viral because it condenses a tension that many families feel under their skin: the duty to help children colliding with the duty to survive.

Some will say the son has behaved irresponsibly. Others will repeat that the real scandal is a labour market that pushes forty-year-olds back into the arms, and the pockets, of their parents. Between these extreme positions, there is a grey zone where almost everyone actually lives. People who try, stumble, help, get angry, forgive, sign, regret.

This case forces us to ask a more uncomfortable question: how much risk are we willing to carry, personally, for the failures of an entire system? And above all: when does love become self-sabotage? The debate will go on in TV studios and online threads, but the quiet conversations, around actual kitchen tables, might be the ones that really change future signatures.

| Key point | Detail | Value for the reader |

|---|---|---|

| Hidden risks of acting as guarantor | The guarantor becomes the first target in case of unpaid instalments, even ahead of the primary debtor | Understand the real legal weight of a “favour” before signing anything |

| The emotional trap of family loans | Guilt, shame and love can cloud judgment and push parents to risk their only home | Learn to separate affection from financial decisions without “loving less” |

| Practical protections | Outside advice, worst-case simulations, and strict limits on what you are willing to risk | Gain concrete tools to help relatives without jeopardizing your future |

FAQ:

- Question 1What does it really mean to act as guarantor for a loan in Italy?

- Answer 1It means that if the person who takes out the loan does not pay, the bank or the collection agency can ask you for the full amount, targeting your income and your assets, including your home if it has been pledged.

- Question 2Can the tax authority really auction a pensioner’s primary residence?

- Answer 2In some cases there are protections on a primary residence, but they do not apply to all types of debt and guarantees; if the house has been used as collateral or mortgage, enforcement becomes possible under specific legal conditions.

- Question 3Is there any way to renegotiate or stop an attachment once the process has started?

- Answer 3Sometimes yes: through instalment plans, negotiations with the collection agency, or by contesting errors in the procedure; acting fast and with professional legal support is crucial.

- Question 4How can parents help an unemployed child without risking their house?

- Answer 4By preferring non-guaranteed support: small interest-free loans within what they can lose, temporary housing, help finding work, or directing the child to social services and training programmes.

- Question 5What questions should I ask before signing any guarantee?

- Answer 5Ask how much you would pay in the worst-case scenario, which of your assets can be seized, what happens if your income drops, and whether there are alternative solutions that do not require your guarantee.